Blog

What is a direct secondary fund?

Peter Hammond

Early stage, primary investing is a difficult and risky game.

It’s tricky to identify the traits of successful ventures when leadership often hasn’t been tested and product-market fit hasn’t been ironed out. Successful ventures take time – 10 years is often the first chapter of a company and a timeframe which often means early investor horizons don’t match the company needs.

It’s a mismatch of needs that is giving rise to the secondary fund which is becoming more prevalent in the global VC market. Over the past decade, VC secondary funds have outperformed regular VC funds.

Secondary markets enable liquidity. Liquidity is critical to the health and long term growth and viability of any market. In fact, in most industries the secondary market is often far larger than the primary market. For example the secondary car market is three times larger than the new car market or the volume traded in a listed stock exchange is orders of magnitude larger than the primary capital raising markets.

The same dynamic is occurring in the venture capital markets globally as the timelines to reach a liquidity event have lengthened over the last decade. This trend has recently been exacerbated by institutional investors (banks, insurance companies, family offices, hedge funds, mutual funds) decisions to sell non-core investments and seek short-term liquidity, and senior executives looking to monetize some of their stake in companies before the company has matured enough to go public.

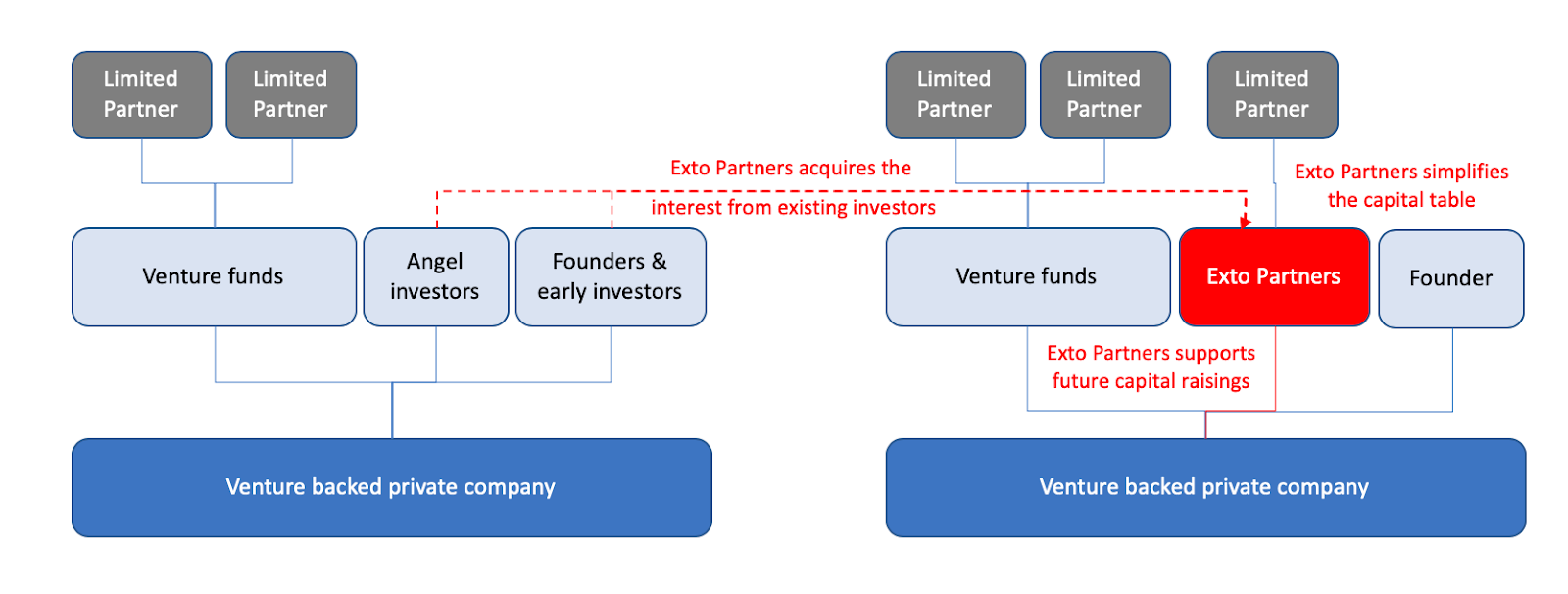

A direct secondary investment refers to the buying and selling of an investor’s ownership in a privately held, venture capital or private equity backed company.

The direct secondary market creates opportunities for current or ex-employees and investors to sell equity before the entire company is sold or becomes mature enough for a public listing. Investors or venture funds often liquidate entire or parts of their holdings in a single company or across an entire portfolio of companies in one transaction.

The journey of any venture business is difficult to predict and often takes many twists and turns as the management strives to find the right team, product-market fit, channel to market and growth. Along the way their investors will also experience changes in circumstances or simply the maturity of a fund. This results in a mismatch between the investment horizon of the investor and the expectations and ambitions of the founder and management team.

In these circumstances a direct secondary transaction makes a lot of sense for all parties. Often the founder and management team are looking to reinvigorate their investor base for future growth opportunities while some investors, who have been on the journey for some time, are often looking for seamless liquidity and return of capital. When this mismatch happens, as it invariably does, investor and management conflict can cause the team to lose focus and miss opportunities.

A secondary transaction can be an important source of liquidity in a variety of situations, including:

| Founders and early employees | Where liquidity timeline is extended |

| Venture funds | With insufficient reserve capital to support portfolio or end-of-life and need to return capital to LPs |

| Early angel investors | Interested in recycling their capital for other investment opportunities or to alter the risk of their retirement portfolios. |

| Corporate VC funds | Wanting to exit their venture investment strategy |

In addition to liquidity, a secondary transaction can clean-up and simplify the capital table by replacing what can be a large number of small, one-time investor angels and ex-employees with one sophisticated investor that will become an ongoing investment partner of the company. Often investors and ex-employees that agitate for liquidity create unnecessary noise for the management team and may even make future capital raising difficult.

How big is the secondary market?

While a robust secondary market for private equity-backed companies has existed for decades, historically, venture capital was too small a segment within the alternative assets class to support a vibrant secondary market.

However, over the past decade, there has been significant growth in the amount of money allocated to venture capital investments. In the US it has grown from $7.4B in 1995 to $28B in 2008 (source: NVCA).

This growth in the venture industry has resulted in a striking disparity between venture capital investments and venture-backed company exits: venture capitalists invested in 31,676 deals between 2001 and 2009, but only 3,164, or 10%, of venture backed companies have had exits in that time period (source: NVCA). This has resulted in the rapid growth in the secondary transactions across the US VC market. The majority of these secondary transactions are undertaken by VC and PE funds that are not dedicated secondary funds but general VC funds.

According to Pitchbook, since 2010, $6.4bn has been invested in 3,195 primary VC deals (across all rounds from angel to late series) by over 1,656 different investors across Australia and New Zealand.

There is a rapidly growing demand for secondary transactions in the Australian and New Zealand markets and this will grow over the next decade as the Australian VC market matures with a vibrant secondary market.

Talk to us

If you think we could be a great business partner for you, we’d love to chat.